Authored by Adam Taggart via Peak Prosperity,

What will happen next & what to do now…

Welcome to our new readers and a very Happy New Year to everyone!

Now that it’s 2019, we’re going to start the new year here at Peak Prosperity by responding to the wishes of our premium subscribers and making our most recent premium report free to everyone.

For those unfamiliar with our work, it’s based on the idea that humanity is hurtling towards a disaster of our own making. Several powerful and unsustainable trends are all converging towards an ever-narrowing gap in the future.

Because of this, the individual and collective choices we make today take on ever-increasing importance. Our collective choices — around such issues as rampant money-printing by central banks, the failure to wean ourselves off of fossil fuels, and tossing an entire younger generation under the bus because that’s most convenient for an older generation afraid of living within its actual means — are all pointing to a diminshed and disappointing future. We need to make better choices that align ourselves with these (and many other) looming realities.

This is our work here at Peak Prosperity.

For ten years now, we’ve been pointing out the many predicaments society faces. And we will continue our vigilance. No because we enjoy crisis, or that we relish delivering hard messages, but because these are the times in which we live — and those, like you, who are awake to reality, need unvarnished facts and data to make informed decisions.

So we offer to you, today, a peek behind our premium subscription curtain. The people who subscribe to our work do so to make themselves more resilient, as well as to support Peak Prosperity financially as we carry on our mission of “Creating a world worth inheriting”, which invoves bringing difficult messages to reluctant audiences. It’s not the easiest work, but someone has got to do it. And we’ve willingly taken that responsibility on.

If you like the idea of being kindly but persistently nudged towards greater personal resilience, and you want to support bringing this message to the world, then please become a premium subscriber to PeakProsperity.com. Join our growing community, and make your money count towards a building a better future for as many people as we can.

~ Chris Martenson

2019: The Beginning Of The End

For ten long years, the world’s central banks have dragged everyone along for one last attempt at scaling Mount Credit.

At several points along the way, in 2011, in 2013 and then again in 2016 it seemed all but certain that the wrong route had been picked and all was lost. We warned people then about the risks, but to no avail. They found a way to navigate even higher from there.

And here we are again in 2018, warning everyone of the same risks. Starting back in August of 2018 we were questioning whether “it” had arrived and then were declaring that it had throughout October and November.

“Until and unless” the central banks reverse course 2019 will see even more of the same. More stock market volatility, more bond losses, and falling real estate. Eventually these credit stresses will impact those portions of the economy dependent on continued access to more dumb money.

Weak companies that cannot sustain themselves without borrowing more will go out of business and lay people off. Major corporations seeing that writing on the wall will reel in their own hiring and expansion plans.

Eventually all the of the highly leveraged trading strategies have to pack up shop and go home and that’s when we discover that these “markets” are as fake as a spray on sun tan. No actual liquidity, only the appearance of such as temporarily afforded by all the computer algos out there.

In a very successful attempt at holiday season humor, the Wall Street Journal finally noted that the equity markets had become dominated by computer algos, a fact we noted – oh – 7 years ago:

Behind the Market Swoon: The Herdlike Behavior of Computerized Trading

Dec 25th, 2018

Behind the broad, swift market slide of 2018 is an underlying new reality: Roughly 85% of all trading is on autopilot—controlled by machines, models, or passive investing formulas, creating an unprecedented trading herd that moves in unison and is blazingly fast.

“Electronic traders are wreaking havoc in the markets,” says Leon Cooperman, the billionaire stock picker who founded hedge fund Omega Advisors.

Behind the models employed by quants are algorithms, or investment recipes, that automatically buy and sell based on pre-set inputs. Lately, they’re dumping stocks, traders and investors say.

“The speed and magnitude of the move probably are being exacerbated by the machines and model-driven trading,” says Neal Berger, who runs Eagle’s View Asset Management, which invests in hedge funds and other vehicles. “Human beings tend not to react this fast and violently.”

(Source)

That’s funny! 10 years of steadily rising “markets” driven by these algos and the WSJ was entirely unconcerned. Now that stocks have been shown to also go down, suddenly the impact of these algos is very concerning to the WSJ. No worries as long as these programs are whipping prices higher, but a lot of concern when they amplify the moves down.

Well, better late than never.

Our concerns about “markets” so dominated by trading programs are that they are too easily subject to (1) manipulation and (2) sharp sudden movements that could, someday, result in markets being shut down due to lack of participation because the algos found conditions “out of parameter” and they up and left in the literal blink of an eye.

If we needed any further confirmation of just how dangerously volatile the markets can be when driven by these automatic trading routines, then Christmas week certainly provided it.

On Christmas Eve the US stock markets dropped more than they ever had. Then the day after Christmas the Dow went up more points than it ever had. The next day it swung an additional 900 points, and rather violently upwards mainly in the last 1.5 hours of trading.

From oversold to overbought to oversold to overbought all in 48 hours.

This is akin to what happens to a car that enters a skid and an inexperienced driver first over-corrects one way and then another with each oscillation become larger and less controllable. Eventually the car lands in a ditch and the ride is over.

Is this happening now? We think so.

And it’s the perfectly natural and expected outcome of too many years of increasing central bank intervention aimed at preventing the very thing we now face.

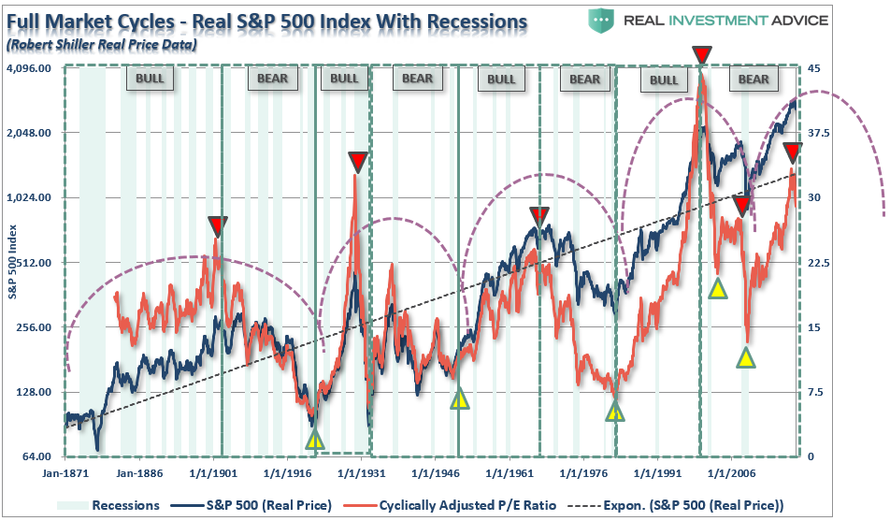

Again, this chart explains everything we have been experiencing in financial “markets” (now so grotesquely distorted by such interventions that price discovery has been almost entirely destroyed):

In every case so far, every attempt to halt QE has resulted in a Wall Street hissy fit and a lot of crybabies in the investing world demanding that the central banks reverse course. And each time they did, and it worked for a little bit longer.

So here we are, and everybody wants to know what comes next.

That’s easy. Until and unless the central banks reverse course, once again, and make the next round of QE even larger and more bigly than any previously, we’ll see lots of declines in financial asset prices. Only this time? It won’t be constrained to falling stocks – it will envelop everything.

A Fed Too Far

Crass, and vulgar, and utterly indefensible. That’s the only way to describe the combined “leadership” of Ben Bernanke and Janet Yellen who conspired to throw an entire generation under the bus, along with the elderly on fixed incomes and savers too.

Millennials were locked out of first time homebuying by an interventionist Fed that decided all on their own that those already living in houses should be made to feel wealthier by virtue of rising home prices.

Instead of noting that the 2001 – 2007 housing bubble was a very bad idea, the Fed printed up $1.75 trillion of fresh money to buy mortgage paper and help drive house prices right back up towards their silly, ill-advised peak.

Houses, over the long term, should appreciate in line with inflation, no more no less. Anything above that green box means house prices have gotten ahead of themselves, and below means they’ve fallen too far.

But the Fed decided, all on its own, that the prior peak was a good thing and needed to be replicated as soon as possible.

The idea here was morally bankrupt as it was illogical. The Fed thought that people living in houses with rising prices would experience a “wealth effect” and therefore both borrow and spend more, which would somehow be a good thing.

The illogical part is not hard to work out. If you are already living in a house, and you have to live in one anyway, are you truly wealthier if it goes up in price? Obviously the answer is no, and a tiny bit of thought reveals the opposite.

The only way to tap that wealth, without borrowing against it, would be to sell your expensive house and downsize or move away to a cheaper location. Moving nearby to an equivalent house does nothing for you expect waste realtor and other transaction fees. A more expensive house defeats the strategy entirely.

Otherwise, living in a more expensive house costs you more in terms of insurance and property taxes. That is, it makes you poorer, not wealthier.

Only in stupid-banker land does a liability that drains more cash from your pocket count as an asset. As Robert Kiyosaki has stressed in every lecture he’s given over the past 25 years, the house you live in is not an asset.

Roofs need replacing, electricity and oil are consumed, painting and mowing and plowing are all part of simply preventing this thing from rotting straight away into the ground. Mortgage interest, insurance and property taxes have to be paid or you will quickly lose ‘your’ house to some authority or another.

You see any cash flying into your pockets during any of that? Me neither.

Therefore your house is a liability. Assets are things that put cash in your pocket, liabilities take cash out. I don’t know about you, but my house is far from perfect except when it comes to taking cash out of my pocket. There it’s batting 1.000

Hence, Robert Kiyosaki is right; the house you live in is a liability, not an asset. How does someone become richer if they borrow more against their money pit? Well, that’s the entire centerpiece of the Fed’s decision to drive house prices up. It makes you richer. That’s their whole plan, laid bare.

Now a cash flowing rental property, either residential or commercial, is another matter entirely. Those areassets. Lever up for those! Borrow away. We’ll be holding a Real Estate investing webinar in January so keep an eye out for that and be sure to sign up.

The immoral part of the Fed’s decision to drive up house prices has two parts. The smaller part concerns the immorality of encouraging people to go deeper into debt (refi’s, HELOCS, etc.) by leveraging a liability. Bankers not should but do know better.

The larger part centers on forcing an entire generation (e.g. Millennials) to either skip buying a house because they can’t afford one, or to buy a more expensive house than they can reasonably or comfortable afford.

Put simply, the Fed threw an entire generation under the housing bus just so that the older folks could feel a little better about the price of their already purchased and lived-in home and maybe spend a little more. It’s no different than setting your house on fire because you are a tiny bit cold.

This was crass, and vulgar, and utterly indefensible.

It’s Over

After ten long years of steadily rising equity markets, or ““markets”” as we like to call them to denote their fictitious and often fraudulent nature, something approximating volatility has returned here very late in 2018.

As we head into 2019, we’re expecting to see a lot more volatility and even more losses as reality once again steps back into vogue. It never really left, of course, only was kept away for a while with monetary Botox administered by self-delusional bankers and politicians unable to face their many failures directly.

Every recovery eventually ends and this one is no different.

In our view, however, any recovery built on a foundation of cheap credit will not only end but end badly. This is easy to understand in neighborhood terms.

Suppose you and your neighbor both earn $100,000. Next year you both still earn $100,000 but your neighbor borrows an additional $25,000 on their credit card to spend on things like a gardener, a boat, and a couple of trips.

The way the government records things your neighbor had their personal economy expand by 25% and that’s a very good thing. Neither the US government nor the Federal Reserve bother to back out the borrowing when they count up economic activity.

Of course, they should, because all borrowing really represents is future consumption taken today. Your neighbor, when they have to pay back that $25,000, plus interest, will have to forego that amount of future consumption to pay back the debts.

How dumb is it to not factor out borrowing when considering economic activity? Fantastically dumb.

Here’s what happens to US GDP growth when just the increase in the federal debt is taken out:

This is why the ‘recovery’ is not really a recovery. It’s not based on anything organic or healthy. It’s simply borrowed and all borrowing sprees eventually come to an end.

Looked at from a stock market perspective, here’s what central bank inspired credit cycles look like:

Or we could rotate it and look at it from the perspective of debt accumulation:

(Source)

The above chart is a head scratcher. Whenever that line is moving upwards, it means that debt growth is outpacing economic growth (and remember, debt’s effect on GDP is not factored out, so it’s even worse than what you are seeing here).

What’s the plan here? Continue to pile up debt at a faster pace than economic growth forever? What about the idea that economic growth has slowed of late and cannot grow forever for resource related reasons? Is anybody in power paying even the slightest bit of attention?

Most importantly, what happens when ~40 years of excessive debt accumulation comes to an end? Do financial systems and institutions even function anymore?

Nobody has a good answer to those questions, which is why the Federal Reserve, et al., are terrified to find out what happens when their grand debt bubble experiment comes to an end. Mad max is not out of the question folks. A lot of things very suddenly no longer work when the credit not only dries up, but goes in reverse. Very basic things like food and gasoline distribution networks and public safety payrolls become difficult to maintain. Just ask Venezuela.

Until and unless the central banks do something very, very different in the months ahead, it’s over.

First They Came For…

Because of just how dire it might be to end a 40 year long, and very ill-advised credit bubble, we are 99.98% certian the central banks will fight tooth and nail to keep it going. Just a little longer, for as many months or years as they possibly can, but they’d kick the can forever if they could.

Meanwhile, the ecological world continues to hurtle towards complete disaster. This next piece of news is one we’ve covered before, but it’s once again in the headlines with some new, rather dire findings:

Building blocks of ocean food web in rapid decline as plankton productivity plunges

Dec 22, 2018

They’re teeny, tiny plants and organisms but their impact on ocean life is huge.

Phytoplankton and zooplankton that live near the surface are the base of the ocean’s food system. Everything from small fish, big fish, whales and seabirds depend on their productivity.

“They actually determine what’s going to happen, how much energy is going to be available for the rest of the food chain,” explained Pierre Pepin, a senior researcher with the Department of Fisheries and Oceans in St. John’s.

“Based on the measurements that we’ve been taking in this region, we’ve seen pretty close to 50 per cent decline in the overall biomass of zooplankton,” said Pepin. “So that’s pretty dramatic.”

Scientists say local testing reveals half the amount of plankton in a square metre of water today. It’s not just a problem here, declining plankton numbers are a global phenomenon.

(Source)

What scientists have been recording is an enormous drop in the very bottom of the entire food pyramid in the oceans of the world. I cannot state this strongly enough; this is frightening and deserves our very highest and collective attention. I cannot think of news much more alarming than a pronounced and continuing loss of oceanic plankton.

One does not simply wipe out the bottom of the oceanic food chain without consequences!

First they came for the insects, but I didn’t realize that they were important because I hate mosquitoes and didn’t really pay attention during biology.

Then they came for the phytoplankton and zooplankton, and, well, same reasons.

Then they came for all the fish in the ocean, but I switched to chicken, so no big deal, right?

Then they came for my oxygen and then it was too late…

On my recent trip to Costa Rica I leaned that even there, where it sounded vibrant and alive to me, that the insects have also begun to mysteriously and quietly disappear, mirroring the hyper-alarming decline in insects noted elsewhere across the world.

What’s going on?

Nobody really knows and I doubt anybody will ever be able to say for sure. The natural world is a complex system with a seemingly infinite number of feedback loops in play.

But one thing we could immediately do is realize that whatever it is that we’ve been doing over the past 25 years that’s new should be stopped right away.

Any pesticides or new chemicals being used should be withdrawn from the market immediately. That would be a sane and healthy response.

Instead the entire political and economic structure of the world is hyperventilating about creating more growth, getting stock prices to go back up, and generally acting as if human developed economic and monetary abstractions were themselves more important than anything else including reality.

So even if the central banks fold and “win the battle” by getting stocks and bonds to resume their march higher, they will assure that we “lose the war” by distracting the center mass of humanity with dreams of riches that will serve to deflect attention from the many predicaments that we face.

We Might be Wrong But We’re Not Confused

That’s one of my favorite sayings; I might be wrong, but I’m not confused.

We’re as certain as can be that the insects and oceanic plankton are sending very important signals to those who can see them. We know that one cannot borrow more than one earns forever. We know that steep and rising wealth and income gaps are socially destabilizing. We know that there’s a future energy crisis coming for which the world is utterly unprepared along every dimension including transportation and food production.

These thing matter, and they will matter more and more as time goes on.

We’re not even the slightest bit confused about any of that.

Hopefully the signs are clear enough again that more people can get back on the path of preparing themselves for the coming times. There will be disruptions aplenty, and we will all know people, perhaps intimately, who are not prepared.

People will lose jobs and investment savings. Many more will lose hope and thereby join a surprising number of young people who already have lost hope themselves.

Losing hope is a great first step. We don’t need any more hope. We do need optimism and we do need new actions, which means we need new belief systems and, of course, all new narratives.

Once we accept where we are and the path we’re on, then we can begin the long process of building resilience into our lives and communities.

But first you have to take care of yourself. You place the oxygen mask over your mouth and nose before attending to those around you and helping them get theirs in place.

As we enter 2019, I want to offer you renewed encouragement to getting yourself prepared. Our basic list should be like basic hand gun training. You cannot over-train on the basics!

Step 1: Make sure your wealth is safely managed or entirely out of the markets. Our endorsed financial advisor uses a variety of hedging techniques to manage risk on existing positions to both limit downside as well as generate some additional returns. Keeping money in cash in the system to us means using TreasuryDirect in part to keep your cash in the safest of all possible places – with the US Treasury. If the Treasury fails, well, then we all have much bigger problems to contend with.

Step 2: Have at least 3 months in cash on hand, and out of the banking system.

Step 3: Have at least a 10% position in physical gold in your hot little hands stored somewhere safe where you can get to it yourself, possibly quickly.

Step 4: Check your supplies. Be sure to have all the basics safely stored and readily accessible. Food, water, personal protection, medical supplies, etc. Just in case of supply disruptions but also to give you peace of mind that will free you up for step 5.

Step 5: Be ready to help. The most likely outcome of all this, by far, is just a grinding decline that causes people to lose jobs and hope. Your role, as one who is prepared, will be to offer support. As much as you can.

To move beyond the basics, and to meet your fellow tribe, consider coming to this year’s Peak Prosperity seminar to be held April 26th – 28th in Sebastopol CA (link to more information here).

Remember, you cannot be too prepared, nor train too much.

Conclusion

Few are ready to hear these messages. More will be ready over the coming year, but still the numbers will be surprisingly small.

This makes it even more important that we stick together and offer each other support and encouragement as we navigate increasingly difficult waters over the coming months and years.

We will all face setbacks. Money will evaporate, jobs might be lost, and opportunities will vanish and appear in brand new places. Our greatest assets will be intangible, and measured in our abilities to adapt quickly, and to be less reactive to events.

40+ year-old credit bubbles to not end either easily or gently. Everything that people think they know about how things work, especially in finance and economically, will be ripped apart.

Eventually we revert to how things were all through history before the great credit wizards got their hands on the levers. Capital is built up slowly from the efforts of humans, and banking and finance will be small portions of the overall activity, no more than 5% of the pie, dedicated to safely moving capital from A to B.

Between here and there? A world of pain as expectations are forced back down to reality. If we’re lucky that happens over many decades in a fairly predictable glide path.

If we’re not lucky, then it happens rather suddenly, or in a series of short, sharp shocks like a bowling ball falling down a set of stairs. That could be a war in the middle east that drives the price of oil over $300/barrel, or a gigantic financial crisis that closes financial borders and causes one or more currencies to utterly fail (I’m looking at you Japan!).

Or a pandemic, or a solar EMP. Who knows? In a world of interdependent, just-in-time delivery systems anything that disrupts the supply chains for more than a month will be the same as our bowling ball skipped three stairs before landing extra hard on the fourth.

Is any of this certain or guaranteed? No, of course not. They are merely probabilities. Smaller in the past, larger today, and growing.

Yes, the authorities will do everything in their considerable power to prevent economic reality from rising up and taking over. They will print, and then print some more.

But they cannot print up 300% more insects to replace those already lost. And they cannot print up 100% more phytoplankton either. Nor can they print up another 100 feet of water column in the Ogallala aquifer.

All they can do is print up more debt and consumption today, stealing from an ever more uncertain future. Can they do it one more time? Probably. Another two times? Three? When does it ever stop but when reality overtakes the whole mess and destroys the works of man?

Which means the most important question before any of us is, what did you do about it?